Apple Grace (not her real name) bought her first home 2 ½ years ago for $1,000,000 in a suburb north of Sydney. She took out a loan of $800,000 and was able to fix her loan at 1.98%. That was January 2021, the pandemic’s 2nd year when the cash rate was at its lowest at .10%. In 6 months, this fixed rate will expire and Apple wants to know what her repayments will be today. She’s worried about how high her repayment will be from the current $2,949 per month she is currently paying.

We did a home loan review based on what her existing bank will offer if the rate were to expire today. Her bank’s variable rate is currently sitting at 7.10% and her loan balance has gone down to $768,000. For the loan term, we’ve set this to 27 years.

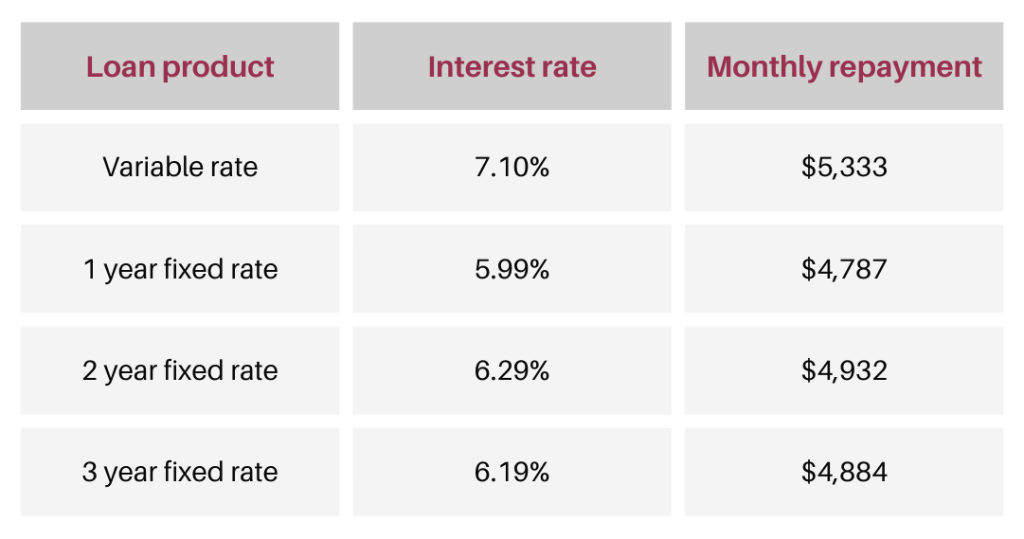

Apple Grace’s current fixed rates with her existing bank are as follows:

- 1-year fixed rate: 5.99%

- 2-year fixed rate: 6.29%

- 3-year fixed rate: 6.19%

With these rates, what does her monthly repayment look like?

It shows from the table that Apple Grace’s repayment will go up by $1,838 if she chooses the 2-year fixed rate and to $2,384 once her fixed rate switches to variable.

Apple Grace wants to explore options of obtaining a lower variable rate than the 7.10% offered by her existing bank. Additionally, she wants to find out if splitting her loan into a fixed and variable portion makes sense. Let’s delve into her scenario and evaluate potential solutions.

Background Information:

- Her 3-year fixed rate of 2.09% is about to convert to a variable rate of 7.10%.

- Loan balance: $768,000

- Property value: $1,100,000

- Loan-to-value ratio: 69.81% (loan balance divided by property value)

Exploring Lower Variable Rates

Apple Grace is seeking a lower variable rate than the 7.10% offered by her current bank. To achieve this, she can consider the following options:

- Research Other Banks and Lenders: Apple Grace can explore other financial institutions to compare their variable rates. It’s crucial to review the interest rates, loan features, terms, and conditions offered by different banks. This comparison will help her identify potential lenders with more competitive rates.

- Utilize the Services of a Mortgage Broker: A mortgage broker can assist Apple Grace in finding the best rates available in the market. They have access to a wide range of lenders and can offer personalized advice based on her financial situation. Working with a mortgage broker can simplify the process of finding a lower variable rate.

- Negotiate with Her Existing Bank: Apple Grace can contact her current bank to negotiate a lower variable rate. Given her history as a customer, the bank may be willing to provide a more favorable rate to retain her business. It’s worth exploring this option before making a decision.

Splitting the Loan

Fixed vs. Variable

Apple Grace also wants to explore the possibility of splitting her loan into a fixed and variable portion. This strategy can provide benefits for both rate types. Here’s how she can proceed:

- Determine the Loan Split Ratio: Apple Grace needs to decide how much of her loan she wants to allocate to the fixed and variable portions. She can opt for a 50/50 split or any other ratio that suits her financial goals and risk appetite.

- Compare Fixed and Variable Rates: It’s crucial to compare the fixed and variable rates offered by different lenders for the desired loan split ratio. This will help Apple Grace evaluate the total cost, repayment structure, and potential savings or risks associated with each portion.

- Calculate Monthly Repayments: Once the loan split ratio and rates are determined, Apple Grace can use an online loan calculator or consult a financial professional to calculate the estimated monthly repayments for both the fixed and variable portions. This analysis will provide a clear understanding of her future financial commitments.

Watch this video for more information about Variable and Fixed rate.

Apple Grace has several options to consider when reviewing her expiring 3-year fixed rate home loan. By exploring alternative lenders, leveraging the services of a mortgage broker, or negotiating with her existing bank, she can seek a lower variable rate than the 7.10% offered. Additionally, splitting her loan into fixed and variable portions can provide the flexibility she desires. Careful consideration of different rates and loan split ratios, along with calculating monthly repayments, will help her make an informed decision regarding her home loan. Remember, it’s essential for Apple Grace to consult with a qualified financial professional or mortgage broker to evaluate the suitability of these options based on her individual circumstances.

Maria Papa is a senior property and finance expert specialising in home loans, investment loans, self-employed loans, alt doc loans, car loans, personal loans, and loan protection. She has offices in Sydney, Melbourne, and Manila. If you have questions, you can call Maria at 0430 144 008 or email her at mpapa@maverickfinance.com.au.